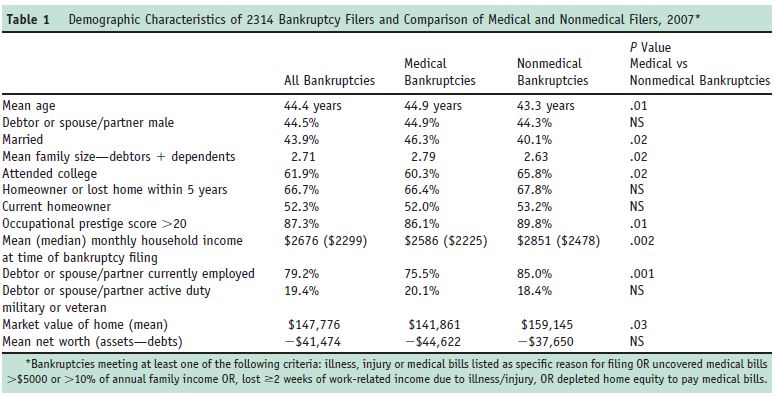

In 2001, a Harvard Medical study found that at least 46.2% of all bankruptcies were due to medical problems and their associated costs. Naturally it should not surprise anyone that between 2001 and 2007 when the study was revisited that percentage increased. The amount itself was pretty shocking – it rose to 62.1%.

Even more shocking were the numbers behind that figure:

- Most medical debtors were well educated, owned homes, and had middle-class occupations.

- 75% had health insurance.

Compare this with 1981 when only 8% of families filed for bankruptcy due to medical issues.

Now that we are 6 years into “Obamacare” – has that number changed? And considering the uncertain future of that program what can we expect from health care costs?

The Effect of the Affordable Care Act on Medical Bankruptcy

Turns out, the Affordable Care Act hasn’t done much to reduce the rate of bankruptcies caused by medical issues. In 2013, NerdWallet studied the effects of the ACA and found that 57.1% of bankruptcies were because of medical costs.

Remember that in the 2007 study, most of those who filed for bankruptcy had health insurance. Its obvious that more people have health insurance now, only ~11.9% of Americans ages 18 – 64 are uninsured.

So what gives? More people are insured, yet medical bankruptcies still remain high. Are people really buying the insurance that they need and are they saving for the costs that they are responsible for?

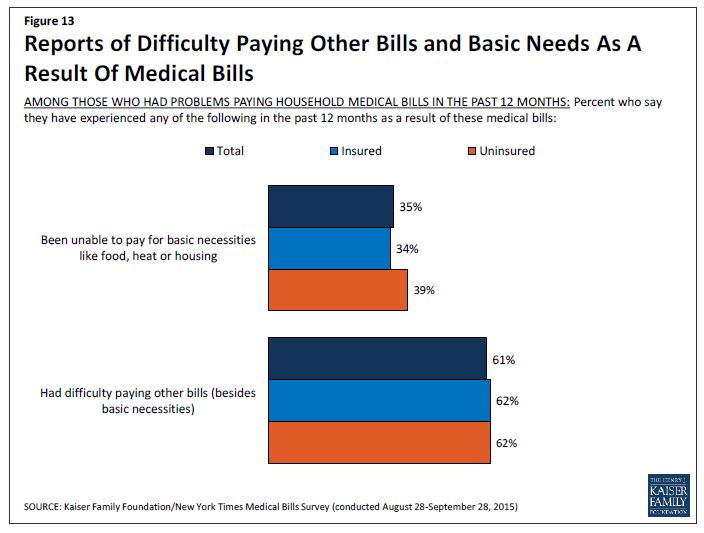

We always assumed that having health insurance would protect us against financial hardship. However, it seems that those who are insured seem to have just as much difficulty paying for other costs as a result of medical bills:

The interesting part here is that those who are insured had just about as hard a time paying for bills as the uninsured. This leads us to the conclusion that just because you are insured doesn’t mean that you can think that you will be spared having to prepare yourself to pay out of pocket and related medical costs.

Many people who have obtained health insurance under the ACA have found there to be high deductibles, co-pays, and out-of-network charges that can quickly add up and overwhelm a budget that was never prepared for it – chances are they signed up with the most affordable insurance plan regardless of those extra costs.

In either event, people need to be prepared for higher medical costs and the related costs to being sick including loss of employment income.

How are people paying for medical bills?

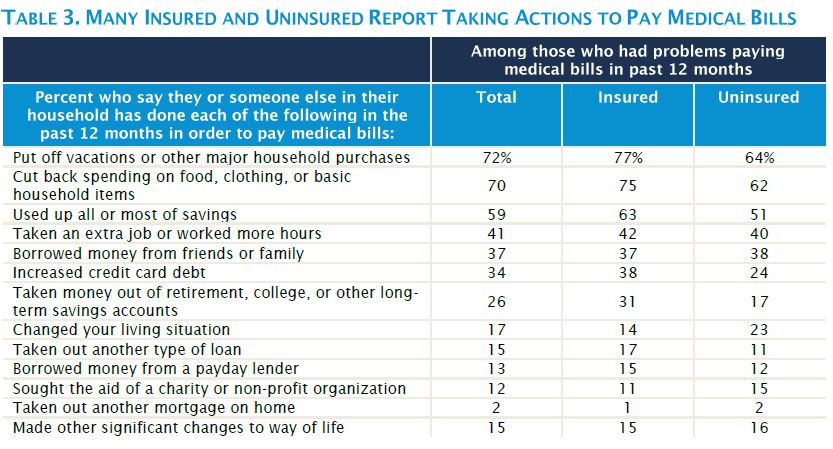

Those who are not prepared for these costs often resort to paying the bills in very undesirable ways according to a 2016 study done by the Kaiser Family Foundation:

Being unprepared in any event can have drastic consequences for your financial future. Turns our that those who were insured actually had to make greater sacrifices than the uninsured! Among the insured – 63% used up all of their savings, 37% borrowed money from friends and family, 15% went to a payday lenders, and 31% took money out of their retirement funds. Is this really a situation you want to find yourself in?

Those who do prepare themselves will have a much easier time paying medical bills:

How do I prepare myself for medical costs?

Obtaining health insurance is only a start. Due to the ACA, most retail plans are affordable only due to the higher deductibles, co-pays, and lack of out-of-network coverage. You as the consumer therefore have the responsibility to be aware of these fees and prepare yourself for them.

There are ways to save on medical costs (negotiating fees, bulk-prescription refills..etc). But these suggestions don’t solve the underlying problem of having to pay excess fees in the first place. The only real remedy is to accept the fact that you will need to allocate part of your budget for both short and long-term health care issues that are not covered by insurance.

Preparing yourself for these costs means that you not only have to have that emergency savings in place for short term emergencies and bills, but also need to think long term about medical costs. Investing your money today can lead to protection against adversity tomorrow. There are a few things to look into:

Establishing a Health Savings Account (HSA)

An HSA can assist with paying direct medical costs IF you have a high-deductible health plan. Contributions into an HSA are not subject to federal income tax at the time of deposit, you can invest those funds as you see fit (mutual funds, stocks, bonds, etc.), and you can withdraw those funds tax-free if used for qualified medical expenses. There are some caveats:

- If you do not have a high deductible health plan you will not qualify for an HSA.

- HSA funds cannot be used to buy over-the-counter drugs.

- An HSA can only be used for qualified medical costs – it cannot be used to replace any lost income from your employment as a result of medical issues. Any funds withdrawn for non-qualified medical costs are subject to income tax and a 20% penalty!

- Your HSA will be in a self-directed account. You will be the one deciding how to invest and grow your HSA savings. Any funds not held in savings accounts insured by the FDIC are subject to risk – you may lose a significant amount or all of your savings if you make poor investment decisions. The amount available to you depends largely on your own investing knowledge and ability.

Research your life insurance policies

Life insurance is exactly that – contrary to popular belief, you are able to use it while you are still alive. Beyond being able to safely and steadily build cash value, some policies include provisions that allow you to be advanced part of the face value in case of chronic (i.e. arthritis, Parkinsons, COPD, etc..) or critical (heart attack, cancer, stroke, burns, etc.) illnesses. You are also not required to spend them directly on medical costs, so they can be used to replace lost income. There is no restriction on to how these benefits can be used!

Consider your health care costs as a part of your retirement planning.

The cost of health care and especially long-term care is a major factor in retirement – most seniors will require long term care at some point in their lives and the cost of LTC is not covered by Medicare. Although there are LTC specific insurance plans, they are expensive and therefore not an option for some. Another option is to leverage your life insurance policy to pay for LTC – many policies include the option for a rider that will allow you to advance the face value to pay for LTC.

What does the future hold?

Well – no one really knows. At this point we can safely assume that the ACA will be modified in some form, but to what extent we don’t really know. It would be ignorant of us to think that health care costs will somehow decrease after several decades on the rise. We can only take the above into account, plan for our own health care costs, and not assume that having health insurance alone will solve our health care costs issues.